What Is Happening With Saudi Arabia's June Oil Pricing for Asia

Saudi Arabia may cut its official June crude selling prices to Asia from record levels as spot premiums have eased and demand has cooled after weeks of supply disruption triggered by the U.S.-Israeli war on Iran, according to a Reuters survey of industry sources.

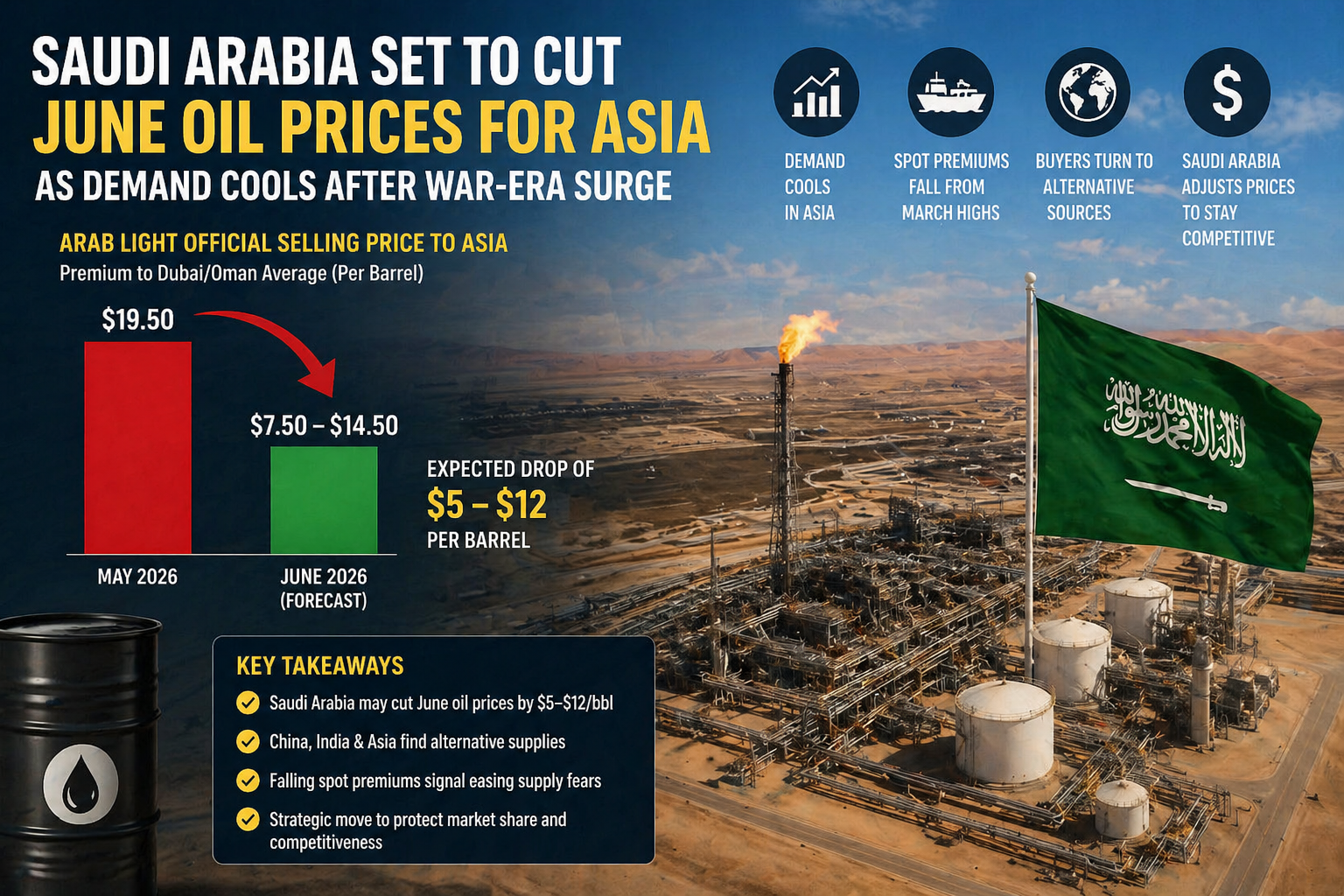

The June official selling price for flagship Arab Light crude may slide to a premium of $7.50 to $14.50 a barrel above the average Dubai and Oman quotes, which would represent a drop of $5 to $12 a barrel compared to the May official selling price. The wide range of forecasts reflects lingering uncertainty among Asian buyers whose crude supply and price expectations have varied since the war disrupted regional shipping.

This is a significant reversal from the peak pricing environment of March and early April 2026, and it tells a much larger story about how energy markets are being reshaped by geopolitical shock, buyer behavior, and the limits of supply-side pricing power.

Who Sets Saudi Arabia's Oil Prices and How the Official Selling Price System Works

Saudi Aramco, the state-owned oil giant of Saudi Arabia, publishes its official selling price each month. The price is adjusted based on the type of crude oil sold, the region where the customer is located, and changes in market supply and demand. Official selling prices serve as the benchmark price for Saudi Aramco to sell crude oil to customers worldwide and function as the main reference price for crude oil in the Middle East.

When setting official selling prices, crude oil products are divided into Arab Super Light, Arab Extra Light, Arab Light, Arab Medium, and Arab Heavy based on density and sulfur content, and then broken out by destination: Asia, Northwest Europe, the Mediterranean, and the United States.

Arab Light, the flagship grade, is the one most closely watched by Asian refiners and market analysts because it anchors a wide range of regional crude pricing contracts.

Why Saudi Arabia Raised Prices to Record Levels in May

To understand the June cut, the May surge needs context.

Saudi Aramco set its May official selling price for Arab Light to Asia at a record $19.50 per barrel premium above the Oman and Dubai average. This was announced on April 6, when Brent crude was trading near $109 per barrel.

That premium reflected extreme supply anxiety. Crude and oil product flows through the Strait of Hormuz plunged from around 20 million barrels per day before the war to just over 2 million barrels per day in March. Exports via alternative routes, most notably from the west coast of Saudi Arabia and the port of Fujairah in the UAE, increased from 3.9 million barrels per day in February to 6.4 million barrels per day on average.

In other words, May pricing was set during a genuine supply emergency. June pricing is being set after markets have begun adjusting.

Who Is Buying Less Saudi Crude and Why

Chinese Refiners Are Pulling Back Sharply

In China, the top buyer of Saudi crude, refiners have been squeezed by weak margins as rising feedstock costs outpaced fuel price hikes, while Beijing has curbed refined fuel exports. Chinese refiners planned to buy just 20 million barrels of crude from Saudi Arabia in May, the lowest volume on record, after the seller hiked its price to a record high.

Sinopec has been drawing on strategic petroleum reserves rather than purchasing Iranian crude at war-era premiums, while simultaneously buying Saudi crude loading from Yanbu and sourcing barrels from outside the Middle East entirely. Sinopec also ordered a halt to new fuel export contracts as of early March, redirecting refinery output to the domestic market and reducing the volume of crude imports needed.

The logic is clear. If Chinese refiners believe Aramco will cut the June official selling price sharply, and the May price's significant premium above current spot gives them reason to expect a correction, then every barrel drawn from reserves today is a barrel bought cheaper next month. Buyers are timing the market, and Riyadh knows it.

Indian and Southeast Asian Refiners Have Found Alternatives

Replacement cargoes from the U.S., West Africa, and elsewhere are expected to arrive from late April, while refiners in India and Southeast Asia have increased purchases of Russian crude under U.S. waivers.

This diversification of supply is structurally weakening Riyadh's ability to sustain premium pricing. When buyers have credible alternatives, sellers must compete.

How Much Did Spot Prices Fall and What Does That Tell Us

The expected price cut follows a sharp weakening in the spot market since late March. The cash Dubai price's premium to swaps fell to $9.17 on Monday, down from a historical high of more than $60 in March after the war hit supply.

Even though there is no end in sight to the conflict, physical crude prices have softened as demand slowed after an initial wave of panic buying.

That phrase is worth unpacking. Panic buying inflates demand signals artificially. When it subsides, the underlying slowdown in consumption, driven by weaker industrial activity and margin compression at refineries, becomes visible. That is what Saudi Arabia is pricing against in June.

What the Pricing Dilemma Looks Like From Riyadh's Perspective

The decision on June pricing is not straightforward for Saudi Arabia. It is a genuine strategic tension between revenue protection and market share defense.

A $10-plus cut for June would be unprecedented and would exceed the volatility range that Asian refinery economics are modeled to absorb. Japanese and South Korean refiners in particular operate on razor-thin cracking margins that assume official selling price stability within a $2 to $3 band month-to-month. A swing of $10 or more in either direction forces inventory revaluation charges that hit quarterly earnings.

In 2014 and 2020, Saudi Arabia had the physical capacity to flood the market since Aramco could produce and export more than 10 million barrels per day if needed. Today, with Yanbu capped at 5.9 million barrels per day of export throughput and 600,000 barrels per day of production capacity impaired by infrastructure attacks, Saudi Arabia cannot flood even if it wanted to. An aggressive official selling price cut would sacrifice revenue on constrained volumes without the compensating benefit of volume gains.

This is a structurally different constraint environment than past price wars, and it makes the June decision genuinely difficult.

What This Means for Asian Energy Markets and Refiners

The International Energy Agency expects 2026 supply to outpace demand by about 3.8 million barrels per day. Lower official selling prices are Saudi Arabia's way of staying competitive when buyers have more options.

When the physical market moves toward surplus, exporters tend to compete on price and terms, and repeated official selling price cuts are one of the clearest signals that pricing power is slowly shifting toward buyers.

For Asian refinery CFOs, a June cut provides some margin relief, particularly for complex refineries in South Korea and Japan that have been absorbing unprecedented feedstock cost volatility over the past two months. For energy traders, it shifts the basis trade dynamic and influences how regional crude benchmarks are priced relative to Brent.

How Saudi Arabia Is Rerouting Exports Around the Strait of Hormuz

Saudi Aramco has been using the Red Sea port of Yanbu to export Arab Light crude after the war restricted shipping through the Strait of Hormuz.

Only Saudi Arabia and the UAE have operational crude pipelines that could potentially reroute flows to bypass the Strait of Hormuz, with an estimated 3.5 to 5.5 million barrels per day of available capacity. Other countries, including Iran, Iraq, Kuwait, Qatar, and Bahrain, rely on the Strait to deliver the vast majority of their oil exports.

This gives Riyadh a structural advantage that most of its Gulf neighbors do not have. However, Yanbu's throughput ceiling is a real constraint, and it limits how much volume Saudi Arabia can actually move at any given price point.