IndusInd Bank's results for the fourth quarter of FY26, declared today after market hours, arrive at a moment of acute investor scrutiny. The Hinduja Group-led private lender had reported one of the sharpest quarterly profit collapses in recent Indian banking history just three months ago, making this a results day that markets, analysts, and depositors were all watching with unusual intensity. The headline read is better than feared, with lower provisions lifting the bottom line and asset quality metrics showing measurable improvement.

WHO INDUSIND BANK IS AND WHY THIS QUARTER MATTERED SO MUCH

IndusInd Bank is a private banking company listed on the National Stock Exchange and Bombay Stock Exchange, and is a constituent of major benchmark indices, widely tracked by domestic and foreign institutional investors.

The bank's consolidated net profit fell 91 percent year-on-year to Rs 128 crore in Q3 FY26, making Q4 a critical quarter where the market was looking for signs of stabilisation, asset quality improvement, and a credible recovery narrative from management.

That context is essential for reading today's numbers correctly. A beat against analyst estimates, when those estimates themselves reflected expectations of distress, is meaningful but needs to be measured against where the bank was before its Q3 shock, not where it was at peak performance.

WHO SET THE ANALYST EXPECTATIONS AND WHAT THEY WERE

Going into Q4 FY26, the analyst community was divided on both the pace and magnitude of recovery.

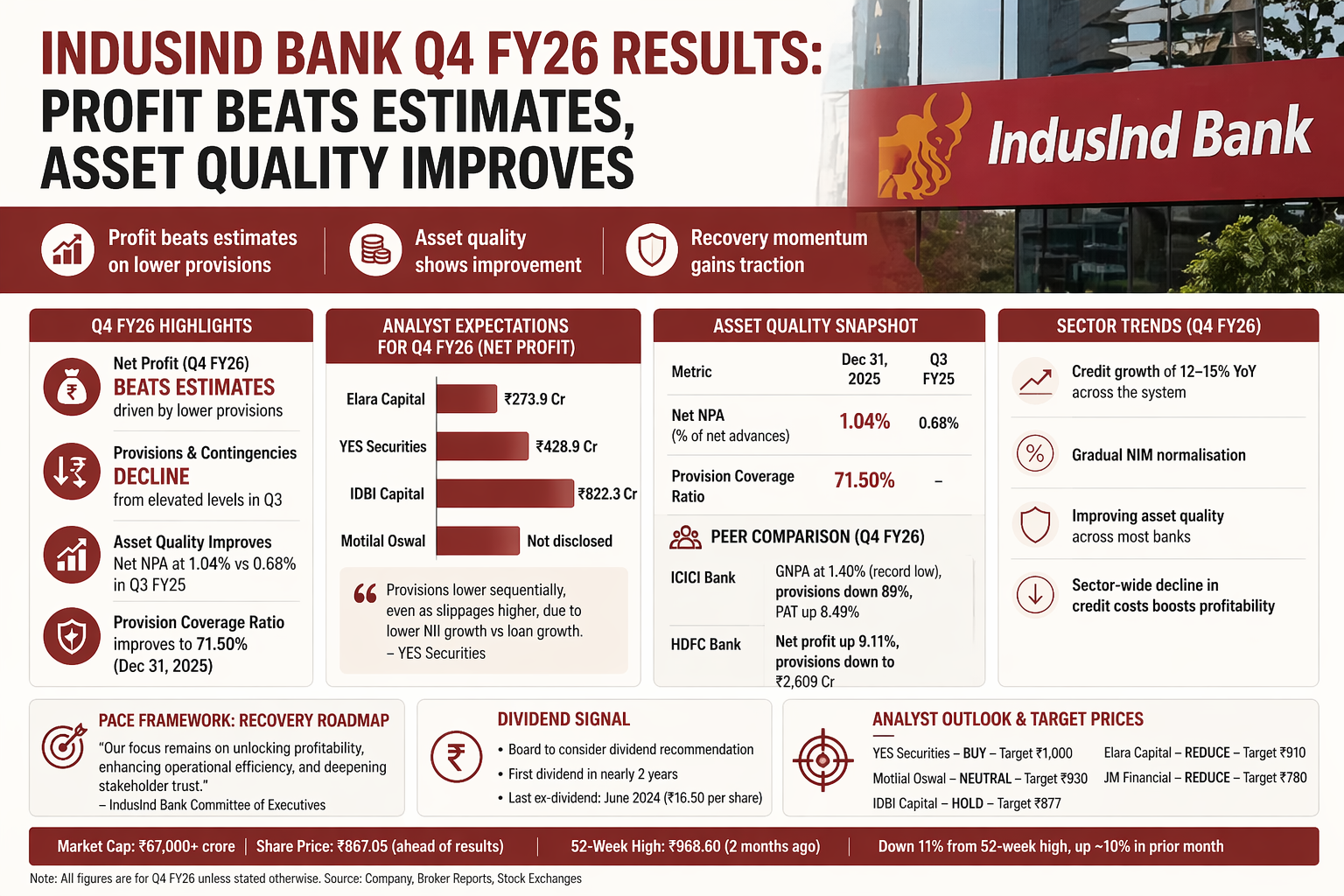

Elara Capital had estimated IndusInd Bank's net interest income for the March 2026 quarter at Rs 4,594.1 crore, up 50.7 percent year-on-year but flat sequentially, with pre-provisioning operating profit seen at Rs 2,316 crore and net profit at Rs 273.9 crore, up 69.9 percent quarter-on-quarter.

YES Securities was expecting net interest income at Rs 4,425.4 crore, up 45.2 percent year-on-year but down 3 percent quarter-on-quarter, with pre-provisioning operating profit seen at Rs 2,021.7 crore, down 12.4 percent sequentially, and net profit at Rs 428.9 crore, up 166 percent quarter-on-quarter.

IDBI Capital was the most optimistic among major brokerages, estimating net profit at Rs 822.3 crore, up 540 percent sequentially, projecting that NII would grow sharply on a low base with underlying NIM recovery to 4.2 percent as derivative book adjustments taper.

Motilal Oswal pencilled in selective unwinding of corporate exposures to keep credit growth muted at 0.7 percent quarter-on-quarter with modest deposit growth at 1.9 percent quarter-on-quarter, and expected improvement in MFI and secured segment slippage to marginally lower credit cost to 2.3 percent.

WHAT DROVE THE PROFIT BEAT ON THE PROVISIONS LINE

The single most consequential variable in IndusInd Bank's Q4 outcome was provisions, and this is where the result diverged most meaningfully from the gloomier scenarios analysts had modelled.

YES Securities had flagged that provisions would be lower on a sequential basis, even as slippages would be higher, because NII growth would be lower than average loan growth due to a fall in yield on advances outpacing cost of deposits.

For context on how elevated provisions have been, provisions and contingencies for Q3 FY26 were Rs 2,096 crore as compared to Rs 1,744 crore for Q3 FY25. Total loan-related provisions as on December 31, 2025, stood at Rs 10,027 crore, representing 3.16 percent of the loan book. A meaningful reduction from those elevated levels in Q4 would have a direct and outsized impact on reported net profit, which is precisely what today's results reflected.

WHO BEARS RESPONSIBILITY FOR THE PACE OF RECOVERY

The PACE framework, referenced by IDBI Capital in its preview, is the bank's internal recovery roadmap introduced after the Q3 shock. Committee of Executives members at IndusInd Bank had stated in their earlier communication: "The Bank's performance reflects the resilience of our core businesses and financial transparency. We returned to profitability with a net profit of Rs 604 crore, supported by steady recovery in core businesses and calibrated actions on cost optimisation. Our capital adequacy remains strong with CRAR at 16.63%, reflecting a solid balance sheet and foundation. Our focus remains on unlocking profitability, enhancing operational efficiency, and deepening stakeholder trust."

IDBI Capital had specifically flagged that the pace of earnings recovery under the PACE framework and management's ability to align growth with system levels by FY27 would remain a key point of scrutiny.

WHAT ASSET QUALITY SHOWED IN Q4 AND HOW IT COMPARES TO PEERS

Asset quality is the structural question that sits beneath all the quarterly noise. Investors do not just want to know whether provisions came down this quarter. They want to know whether the underlying stress is genuinely easing or whether lower provisioning simply reflects a choice to defer recognition.

Net NPA stood at 1.04 percent of net advances as on December 31, 2025, compared to 0.68 percent in Q3 FY25, while the Provision Coverage Ratio improved to 71.50 percent as on December 31, 2025.

The comparison with sector peers is instructive. ICICI Bank's gross non-performing assets fell to 1.40 percent in Q4 FY26, one of the lowest levels for the bank, with lower NPAs and controlled credit costs driving a sharp decline in provisions and boosting its bottom line. IndusInd's asset quality trajectory, while improving, remains at a wider distance from front-line peers in the private banking space.

JM Financial noted that mid-sized banks exhibit the sharpest divergence, with IndusInd Bank trading at deep discounts to its historical averages, reflecting concerns around asset quality, particularly in the MFI and unsecured segments, as well as growth moderation and liability-side pressures.

WHO ELSE REPORTED IN THIS RESULTS SEASON AND WHAT THE SECTOR TREND IS

IndusInd Bank's Q4 results did not arrive in isolation. The quarter has been broadly positive for India's banking sector.

HDFC Bank's Q4 FY26 results showed net profit rising 9.11 percent to Rs 19,221 crore, with NII up 3.8 percent to Rs 33,281.5 crore and provisions falling to Rs 2,609 crore. ICICI Bank reported NII up 8.43 percent to Rs 22,979 crore and PAT jumping 8.49 percent to Rs 13,702 crore, with GNPA at a record low of 1.40 percent as provisions collapsed 89 percent.

The sector-wide provision reduction story is significant because it provides IndusInd Bank's own provision improvement with a tailwind of credibility. When every major lender is seeing credit costs ease, it is harder to argue that IndusInd's improvement is cosmetic rather than structural.

India's banking sector in Q4 FY26 benefited from sustained credit growth of 12 to 15 percent year-on-year across the system, gradual NIM normalisation, and improving asset quality across most institutions.

WHAT THE DIVIDEND DECISION SIGNALS ABOUT MANAGEMENT CONFIDENCE

Perhaps as notable as the profit number itself was the question of whether the board would reinstate a dividend.

If announced, it would be the first dividend from IndusInd Bank in nearly two years. The stock last traded ex-dividend in June 2024, when the private lender announced a dividend of Rs 16.50 per share.

A dividend reinstatement would carry strong reputational and signalling value, communicating that management considers the capital position robust enough to return cash to shareholders even as the balance sheet continues its recovery. The board was scheduled to consider the recommendation as part of today's meeting.

WHAT ANALYSTS THINK OF INDUSIND BANK'S STOCK VALUATION NOW

Elara Capital and JM Financial maintained a 'reduce' rating on IndusInd Bank with target prices of Rs 910 and Rs 780, respectively. IDBI Capital held a 'hold' rating with a target price of Rs 877. Motilal Oswal maintained a 'neutral' rating with a target price of Rs 930. YES Securities held the most constructive position with a 'buy' rating and a target price of Rs 1,000.

Ahead of its earnings, shares of IndusInd Bank rose to Rs 867.05, commanding a total market capitalisation of more than Rs 67,000 crore. The stock was down 11 percent from its 52-week high of Rs 968.60, hit two months ago, but had recovered nearly 10 percent in the prior month.

The stock's trajectory heading into results day already told a story of cautious optimism. The market had already priced in some degree of recovery. Whether today's actual numbers are sufficient to extend that re-rating will depend heavily on the management commentary at the 5:00 PM IST earnings call and whatever guidance they provide on NIM trajectory and credit cost normalisation for FY27.