Governments around the world are now spending more on interest payments than at any point in a generation. The shift is not a footnote in budget documents. It is reshaping national priorities, crowding out public investment, and locking policymakers into fiscal positions they cannot easily reverse.

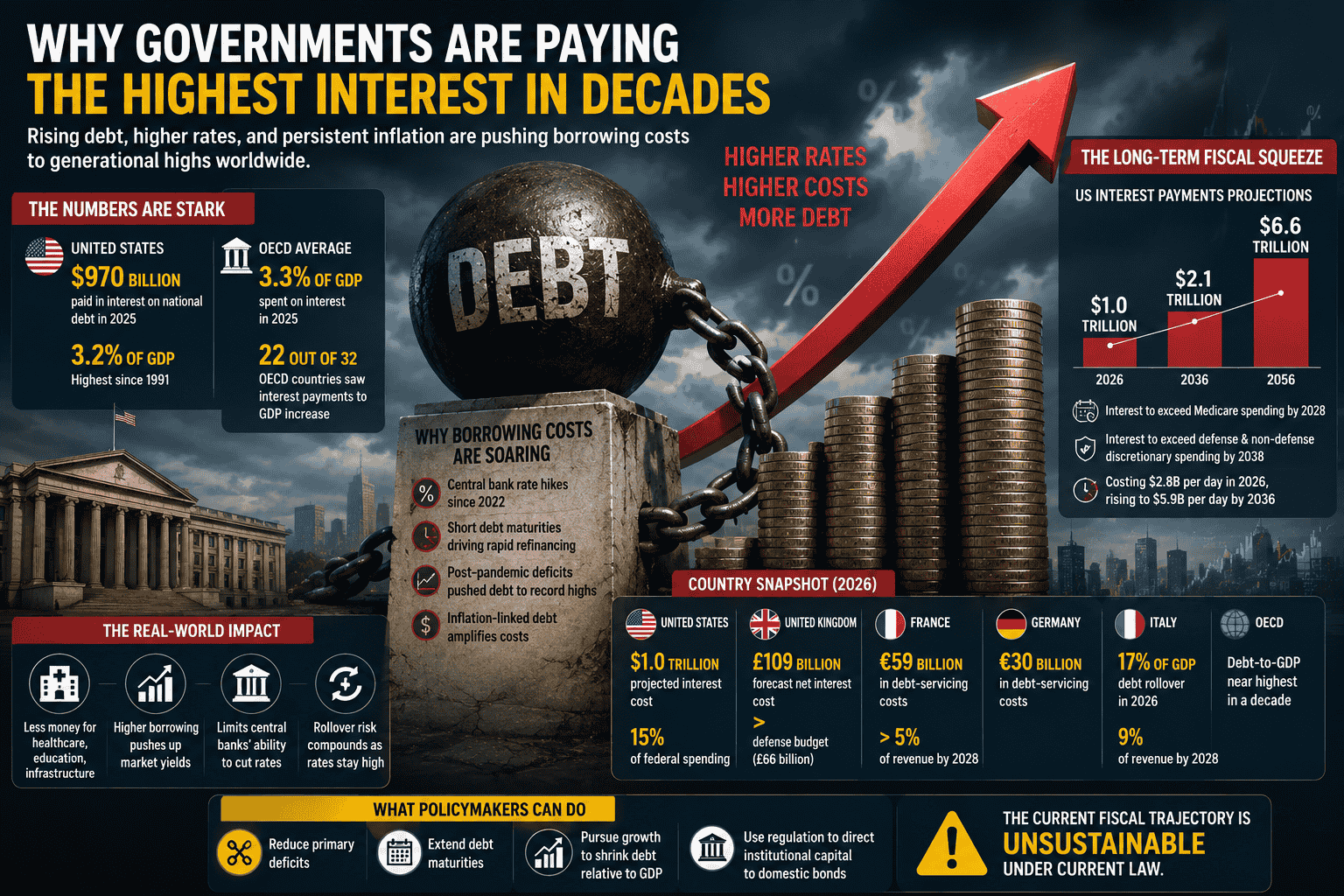

The numbers are stark. The United States paid $970 billion in interest on its national debt in 2025. Relative to the size of the economy, that figure reached 3.2 percent of GDP, eclipsing the previous high set in 1991. And the trajectory is only steeper from here. The Congressional Budget Office projects that US interest costs in 2026 will total $1.0 trillion, a 7 percent increase from the year before.

This is not an American problem in isolation. Across the OECD area, interest expenditures as a share of GDP stood at 3.3 percent in 2025, close to the 3.4 percent peak of the previous decade. Interest payments to GDP increased in 22 out of 32 OECD countries for which data are available.

Why this matters beyond the budget:

- Rising debt service costs reduce money available for healthcare, defence, and infrastructure.

- Higher government borrowing pushes up yields across the broader bond market.

- Persistent fiscal pressure limits central banks' ability to cut interest rates aggressively.

- Countries with short-maturity debt face compounding refinancing risk as bonds roll over at higher rates.

What Is Driving Government Borrowing Costs This High

The short answer is a collision between two forces that rarely coincide this powerfully: accumulated debt and a sustained period of elevated interest rates.

For most of the 2010s, governments borrowed at historically low rates. Central banks kept policy rates near zero after the 2008 financial crisis, and sovereign bond yields followed. Governments issued vast quantities of cheap debt, and the annual cost of servicing it remained manageable. Then came the inflation surge of 2021 and 2022. Central banks responded with the fastest and steepest rate-hiking cycles in decades, and government borrowing costs moved with them.

Most of the outstanding debt in the US in late 2022 was scheduled to mature within three years. That debt has been refinanced at higher interest rates, sharply raising debt service costs. Almost $7 trillion worth of debt was refinanced during fiscal year 2023 alone, and each percentage point increase in interest rates on that refinanced debt added $70 billion per year to net interest payments.

The maturity structure of debt turned a rate problem into a budget crisis.

Key structural factors behind the surge:

- Central bank rate hikes from 2022 onward repriced the entire cost of new and rolling sovereign debt.

- Short average maturities forced rapid, expensive refinancing across major economies.

- Post-pandemic fiscal deficits pushed gross debt levels to multi-decade highs before rates rose.

- Inflation-linked debt in countries like the UK amplified cost increases further.

The debt-to-GDP ratio in many OECD countries by the end of 2025 was close to the highest level in the past decade, with interest payments and inflation identified as the main drivers of debt evolution in recent years.

The Country-by-Country Picture

The pressure is not evenly distributed, but it is broadly shared across advanced economies.

In the United States, the Treasury spent $104 billion in interest in just the first nine weeks of fiscal year 2026, more than $11 billion per week, already representing 15 percent of federal spending. In 2024, federal interest payments surpassed spending on both Medicare and national defence.

The United Kingdom faces a particularly acute version of this problem because of its unusually high share of inflation-linked bonds. Britain was forecast to spend roughly 109 billion pounds on net debt interest in 2026/27, compared to around 66 billion pounds on its defence budget.

Across the Channel, the pressure is building toward structural thresholds. French state debt-servicing costs were expected to reach 59 billion euros in 2026, with Germany's around 30 billion euros. Italy's interest costs were projected to rise to 9 percent of revenue by 2028, according to S&P Global Ratings, while France's were expected to climb above 5 percent as politicians struggle to reach agreement on fiscal policy.

Rollover risk adds another layer of exposure:

- Italy faces a debt rollover equivalent to 17 percent of GDP in 2026, compared to 12 percent for France and 7 percent each for the UK and Germany. Countries that must replace maturing debt at current market rates will absorb higher costs for years regardless of where policy rates eventually land.

What Happens Next: The Long-Term Fiscal Squeeze

The most concerning aspect of the current situation is not where interest costs stand today. It is where they are headed.

The CBO projects US interest payments will grow from $1.0 trillion in fiscal year 2026 to $2.1 trillion in 2036 and $6.6 trillion by 2056. Over the 2026 to 2036 window, interest will grow faster than any other major budget category, increasing by 106 percent. Interest costs are projected to exceed Medicare spending by 2028 and defence and non-defence discretionary spending by 2038.

The US Treasury will pay an average of $3 billion per day in interest in 2026. Under current projections, that rises to $5.9 billion per day by 2036.

These figures represent a structural shift in what governments can afford to do. Every dollar or pound spent on interest is unavailable for schools, hospitals, infrastructure, or tax relief. The compounding effect means that high debt generates high interest, which generates more debt, which generates more interest.

What policymakers can realistically do:

- Reduce primary deficits through spending restraint or revenue increases.

- Extend average debt maturity to lock in current rates before any future spikes.

- Pursue nominal growth strategies that shrink debt relative to GDP over time.

- Use financial regulation to direct pension and institutional capital toward domestic bonds.

None of these options is fast, and several are politically costly. The fiscal trajectory across most advanced economies is, as the CBO's own language states, unsustainable under current law.