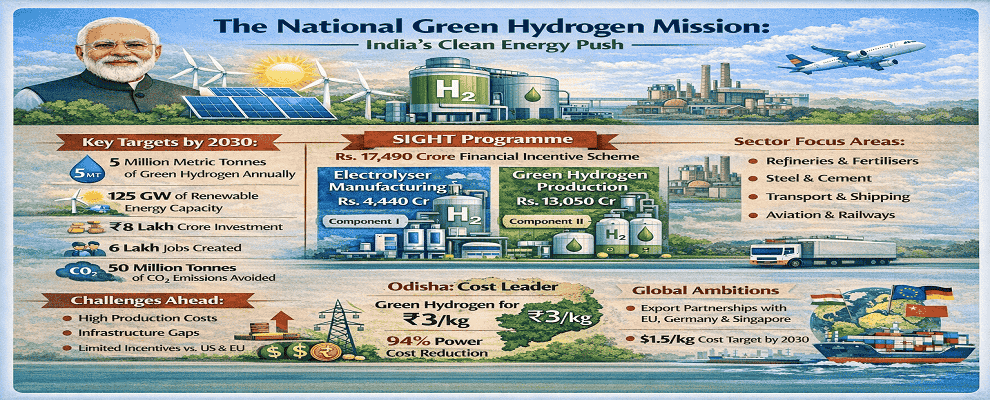

India imports over 85% of its crude oil and nearly half of its natural gas. That single fact explains the urgency behind the National Green Hydrogen Mission, which the Union Cabinet approved on January 4, 2023, under Prime Minister Narendra Modi. The mission is not a peripheral climate initiative. It is a strategic energy security document dressed in the language of decarbonisation, and its targets are among the most ambitious any major economy has set for this technology.

Green hydrogen, produced by splitting water through electrolysis powered by renewable electricity, emits nothing but water vapor. It can decarbonise industries that electricity alone cannot easily reach: steel, fertilisers, heavy transport, shipping, and aviation. India's argument for leading this transition rests on its abundant and rapidly cheapening solar and wind resources, its large domestic demand in hard-to-abate sectors, and the opportunity to become a global export hub for green hydrogen and its derivatives, primarily green ammonia and green methanol.

What the National Green Hydrogen Mission actually targets

The Mission operates under a two-phase structure. Phase I, covering 2022-23 to 2025-26, focuses on creating demand and enabling supply by incentivising domestic electrolyser manufacturing, deploying green hydrogen in existing sectors such as refineries, fertilisers, and city gas distribution, and running pilot projects in steel, mobility, and shipping. Phase II, from 2026-27 to 2029-30, anticipates green hydrogen becoming cost-competitive with fossil fuels and scales up commercial-grade deployment across steel, mobility, railways, and aviation.

The headline targets are production capacity of at least 5 million metric tonnes per annum by 2030, supported by 125 GW of additional renewable energy capacity, total investments exceeding Rs. 8 lakh crore, over 6 lakh jobs, and an annual avoidance of nearly 50 million metric tonnes of CO2 emissions. The government aims to bring production costs down to $1.5 per kilogram by 2030, from approximately $4.4 per kilogram today.

The Mission's initial budget allocation of Rs. 19,744 crore is distributed across the Strategic Interventions for Green Hydrogen Transition (SIGHT) programme at Rs. 17,490 crore, pilot projects at Rs. 1,466 crore, research and development at Rs. 400 crore, and other mission activities at Rs. 388 crore. An additional Rs. 400 crore outlay for Green Hydrogen Hubs is earmarked through 2025-26, with at least two such hubs planned in the initial phase.

SIGHT: the financial engine of the mission

The Strategic Interventions for Green Hydrogen Transition (SIGHT) programme is the Mission's primary financial instrument, functioning as a Production Linked Incentive scheme for the green hydrogen sector. It operates through two components, each implemented by the Solar Energy Corporation of India (SECI).

Component I: electrolyser manufacturing

Component I carries an outlay of Rs. 4,440 crore and runs from FY 2025-26 to FY 2029-30. Its objectives include maximising indigenous electrolyser manufacturing capacity, achieving lower levelised cost of hydrogen production, ensuring globally competitive product quality, and progressively enhancing domestic value addition. In the first tender round, SECI received bids for more than double the 1,500 MW target, with 21 companies proposing a combined capacity of 3,328.5 MW. Eight companies were awarded capacity, including Reliance Electrolyser Manufacturing, Larsen and Toubro, Adani New Industries, and John Cockerill Green Hydrogen Solutions.

Component II: green hydrogen production

Component II carries an outlay of Rs. 13,050 crore and incentivises actual green hydrogen output rather than manufacturing capacity. The inaugural tender targeted 450,000 metric tonnes per annum, but SECI received bids of 551,500 MTPA from 13 bidders, again significantly oversubscribed. Award recipients include Reliance, Greenko, ACME, Torrent Power, JSW Neo Energy, and Bharat Petroleum. As of early 2026, a total of 19 companies hold annual production allocations amounting to 862,000 tonnes, and 15 firms have been awarded 3,000 MW of annual electrolyser manufacturing capacity.

"By leveraging India's advantage in low-cost renewable electricity, the SIGHT program aims to achieve competitive domestic electrolyser manufacturing and reduce the costs of green hydrogen production. The programme has received an enthusiastic response from the industry." — Vibhuti Garg, Director South Asia, IEEFA

Sector applications already underway

Refineries and fertilisers

The most immediate domestic application is substituting grey hydrogen in existing industrial users. 20,000 tonnes per annum of green hydrogen has been awarded for supply to Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum refineries, with an additional 10,000 tonnes per annum allocated to Numaligarh Refinery Limited in Assam. The fertiliser sector is equally significant, with 724,000 tonnes per annum of green ammonia tendered by SECI in June 2025 across 13 fertiliser plants nationwide, awarded to seven green ammonia producers.

Mobility and railways

India completed oscillation trials of its first hydrogen-powered train in early 2026, confirmed by Railway Minister Ashwini Vaishnaw. The train, manufactured entirely by the Integral Coach Factory under the Make in India initiative, features a 2,400 kW power capacity and uses hydrogen fuel cells to generate electricity, producing only water vapor. It will operate on the Jind-Sonipat route in Haryana under Northern Railway, supported by a hydrogen production plant at Jind. Five pilot projects covering 37 hydrogen-fueled vehicles and 9 refueling stations across 10 national routes are also sanctioned. NTPC commissioned the world's highest-altitude green hydrogen mobility project at Leh in November 2024, operating at 3,650 metres with five intra-city buses and a fueling station.

Ports and maritime

A port-based green hydrogen pilot facility was commissioned at V.O. Chidambaranar Port in September 2025, supplying hydrogen for street lighting and EV charging. Deendayal Port Authority at Kandla has commissioned a megawatt-scale indigenous green hydrogen facility with an annual production capacity of approximately 140 metric tonnes. A Rs. 42 crore, 750 cubic metre green methanol bunkering facility is under development to support a Coastal Green Shipping Corridor between Kandla and Tuticorin.

Case study: Odisha - most cost-competitive state for green hydrogen

Odisha has emerged as India's leading state for green hydrogen cost economics. Its incentive package, which includes capital subsidies, electricity charge waivers under the Industrial Promotion Policy, and an additional Rs. 3 per kWh electricity waiver unique among all Indian states, can reduce power costs by up to 94%. This combination brings green hydrogen production costs down to approximately $3 per kilogram, roughly 42% below the national average, making it a preferred destination for large-scale project developers.

International partnerships and export strategy

India's export ambition is backed by a growing portfolio of bilateral agreements. Under the EU-India Trade and Technology Council, over 30 joint research proposals on hydrogen production from waste have been submitted internationally. A Standards Partnership Workshop with the UK in February 2025 focused on harmonising regulations, codes, and standards for hydrogen trade. In November 2024, SECI signed an MoU with Germany's H2Global Stiftung to develop market-based mechanisms and joint tender designs for exporting Indian green hydrogen to international markets. Singapore's Sembcorp Industries signed MoUs with V.O. Chidambaranar and Paradip Port Authorities in October 2025 to develop integrated green hydrogen and ammonia export hubs.

The government has also reduced GST on electrolysers from 18% to 5%, a meaningful cost intervention given that electrolysers and supporting equipment account for nearly 40% of the total cost of producing green hydrogen. A Rs. 100 crore innovation scheme supports startups working on hydrogen production, storage, transport, and utilisation, with individual grants of up to Rs. 5 crore per project.

Challenges that could slow the mission

The enthusiasm from industry is real. The structural barriers are equally real. Using green hydrogen to decarbonise domestic end-use industries remains uncertain due to infrastructure limitations, regulatory ambiguities, and the absence of enforceable consumption mandates. IEEFA analysts noted that most SIGHT winners are likely to focus on export markets in the near term rather than domestic offtake, because domestic pricing and demand infrastructure are not yet aligned.

The incentive gap is significant by international standards. India's initial incentive of approximately Rs. 50 per kilogram, declining annually, compares poorly to the United States, which offers up to $3 per kilogram as a base tax credit under the Inflation Reduction Act, and the European Union, which provides approximately 4 euros per kilogram in high-priority member states. The government's current allocation covers only approximately 40% of the total estimated budget requirement for green hydrogen fuel production.

Infrastructure constraints compound the challenge. A report by the Energy and Resources Institute found that nearly 60% of India's existing hydrogen production infrastructure requires immediate upgrades to be compatible with green hydrogen processes. Land availability, grid readiness, and proximity to demand centres remain binding constraints for standalone renewable-powered projects. Transmission-related charges can raise the landed cost of renewable power to 1.5 to 2.5 times the base generation cost, eroding the economics of grid-connected projects unless state-level waivers are maintained long term.

The SIGHT incentives are time-limited to three years for production and five years for electrolyser manufacturing. Without a credible long-term demand signal from domestic industry, investors face elevated risk in committing capital beyond the incentive window. The definition framework for green hydrogen also needs refinement: globally accepted criteria for additionality, deliverability, and temporal matching of renewable electricity to electrolysis remain insufficiently specified in India's current regulatory guidance.

Where the mission stands as Phase II begins

India is transitioning from Phase I to Phase II of the Mission in 2026, and the ground-level progress is more substantive than most comparable national programmes at the same stage. Production allocations are live, electrolyser manufacturing awards are contracted, port-based pilots are commissioned, the first hydrogen train has completed trials, and international partnerships are operational. The Strategic Hydrogen Innovation Partnership (SHIP), a public-private R&D framework with a dedicated fund, is supporting 23 projects across hydrogen production, safety, storage, and industrial applications.

The cost trajectory is encouraging. Production costs are projected to fall from approximately $4.4 per kilogram today to $2.4 per kilogram by 2030, driven by declining renewable energy costs, scaling electrolyser manufacturing, and infrastructure development. Whether that trajectory is sufficient to make India globally competitive against countries with more aggressive subsidy regimes and more developed hydrogen infrastructure remains the defining question for Phase II.