Why Markets Are Moving and What Is Actually Driving the Optimism

After five brutal weeks of war-driven volatility, global equity markets delivered one of their most decisive relief rallies of the year on Tuesday, and the message from traders could not have been clearer: the single most important variable for financial markets right now is not earnings, not the Federal Reserve, and not tariffs. It is whether the United States and Iran can stop fighting.

The S&P 500 leaped 2.9% on Tuesday for its largest single-day gain since last May. The Dow Jones Industrial Average jumped 1,125 points and the Nasdaq Composite surged 3.8%, as oil prices eased to fuel the rally.

For investors who have watched their portfolios bleed through March, this was not just a good day. It was a signal about what a genuine ceasefire could unleash across asset classes.

What Triggered the Rally: The Reports That Moved Markets

The Wall Street Journal reported on Monday that U.S. President Donald Trump told aides he was willing to end the military campaign against Iran even if the Strait of Hormuz remained largely closed. That single report cracked open a window of hope that markets had been desperately waiting for.

The move came after an unconfirmed report said Iranian President Masoud Pezeshkian was open to ending the war with security guarantees. The S&P 500 gained 2.91% to end at 6,528.52, and the Nasdaq Composite advanced 3.83% to 21,590.63. Each of the three major indexes posted their best single day since May.

Trump also told the New York Post that the Iran war will probably end soon, and separately stated that the U.S. could end its military attacks within two to three weeks, adding "We leave because there's no reason for us to do this."

The combination of those statements, even without formal confirmation from Tehran, was enough to shift market sentiment from fear to cautious optimism almost instantly.

How Asian Markets Responded: The Biggest Single-Day Swings of the Crisis

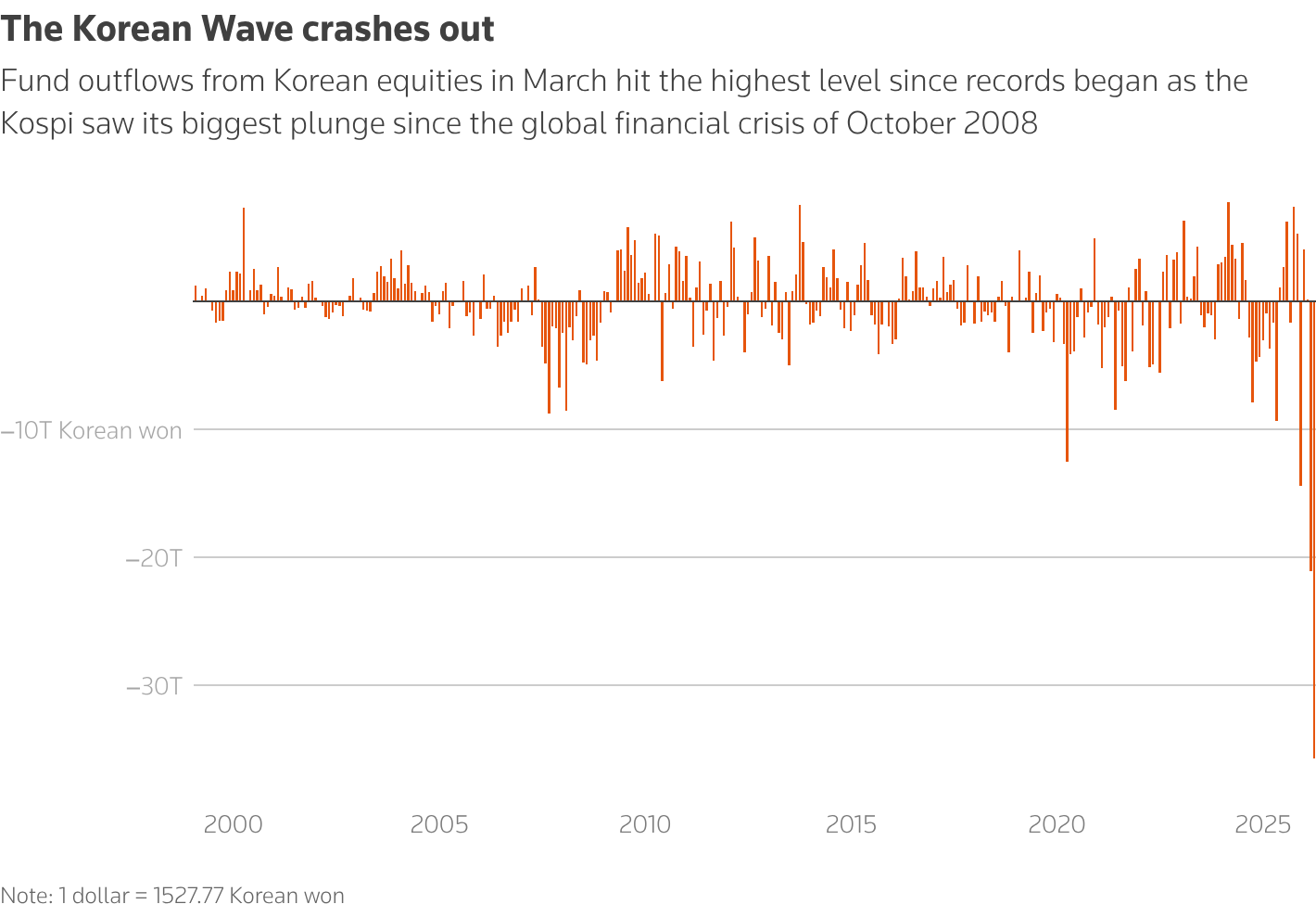

Asia-Pacific markets rebounded sharply on Wednesday, with South Korea's Kospi surging over 6.5% and the small-cap Kosdaq gaining 5.38%, after data showed South Korean exports in March jumped 48.3% from a year earlier, beating Reuters poll estimates of 44.9%.

Japan's Nikkei 225 rose 4.04%, led by financial stocks, while the broad-based Topix added 3.79%. The Bank of Japan's Tankan survey for the first quarter of 2026 showed optimism among large Japanese manufacturers rising to 17 from 15, beating expectations and reaching its highest level since the fourth quarter of 2021.

Hong Kong's Hang Seng index gained 1.71%, powered by basic materials stocks, while mainland China's CSI 300 rose 1.47%.

To understand why these moves were so dramatic, you need to understand how exposed Asian economies are to the energy disruption at the heart of this conflict. South Korea sources about 70% of its crude oil from the Middle East. For Japan, that number is closer to 90%. Any credible signal that the Strait of Hormuz could reopen translates almost immediately into relief across the industrial and manufacturing sectors that dominate these markets.

What the Context Looks Like: A Month of Severe Market Damage

The scale of Tuesday's relief rally only makes sense when placed against the damage that preceded it.

The month-long conflict had left the S&P 500 and the Dow on track for their largest quarterly falls since early 2022. The S&P 500 energy index was the only sector poised to end March in positive territory, logging its biggest quarterly jump on record, tracking a rally in oil prices.

The biggest concern for global stock markets early in 2026 was artificial intelligence. Now, investors' attention has moved squarely to how long the Iran war will last, how much inflation could jump, and what that could mean for the broader economy. Dramatic intraday swings in indexes like the S&P 500 have become common throughout March.

The Kospi fell by over 16% since the Iran war began. Japan's Nikkei 225 and Australia's ASX 200 were down by around 10% and 6% respectively over the same period.

That is the foundation from which Tuesday's rally launched. These were not markets that were slightly bruised. They were markets that had been systematically repriced lower by one of the most significant geopolitical shocks to energy supply in decades.

The Oil Market's Role: Why Crude Is the Central Variable

No single asset tells the story of this conflict more clearly than oil. The conflict caused immediate volatility in energy markets, with Brent crude oil prices surging 10 to 13% in the opening days of the war. Iran's closure of the Strait of Hormuz disrupted 20% of global oil supplies and significant liquefied natural gas volumes.

As February came to a close, drivers in many parts of the U.S. were paying under $3 for a gallon of gas. By late March, the nationwide average topped $4 for the first time since 2022. The jump in diesel was more pronounced, with the average for a gallon reaching $5.45, up from about $3.76 before the war began.

On the day of Tuesday's rally, crude prices fell meaningfully. Brent crude fell more than 4% and traded close to $100 a barrel. Benchmark U.S. crude was down by more than 3.7%, just below $89 a barrel.

Hopes that traffic may be slowly resuming through the Strait were also supported by reports that Iran chose to let a number of vessels pass through the strait, rather than imposing full disruption, according to ship tracking service Kpler.

What Jim Cramer's "Dry Run" Call Tells Us About Investor Psychology

CNBC's Jim Cramer framed Tuesday's session in terms that most professional investors privately agree with.

"Today we saw what would happen when you give peace a chance," Cramer said. "Maybe this dialogue with Iran is really nothing more than an exchange of messages. Maybe it's meaningless. So, consider today a dry run of what will ultimately occur when the war winds down."

Cramer predicted three shifts once the war genuinely ends: interest rates are set to fall, marking a major reversal for the 10-year Treasury; oil prices will drop, removing the inflation premium built into energy markets; and big bank stocks will rally, as the war has frozen Wall Street dealmaking confidence. Tuesday's winners included Goldman Sachs and Morgan Stanley, which advanced nearly 5% and 4% respectively.

That framework matters because it tells us markets are not just reacting to headlines. They are actively rehearsing a post-war repricing.

Why the Rally Remains Fragile: The Risks That Have Not Gone Away

It would be a mistake to treat Tuesday's session as a resolution. It was a reaction to signals, not to facts on the ground.

Iranian officials publicly disputed Trump's claims of ongoing talks. Iran's Foreign Minister Abbas Araghchi told Al Jazeera that negotiation requires two countries engaging in talks to reach an agreement, and said "such a thing does not exist between us and the United States."

The oil spike stemming from the Iran conflict has revived inflation worries, prompting money market participants to price out any Federal Reserve rate easing this year, compared with two cuts expected before the war broke out, according to CME Group's FedWatch Tool.

Alonso Munoz, CIO at Hamilton Capital Partners, described the situation accurately: "What we've seen from a messaging standpoint from the administration is a bit of indication they may start to either wind down or pivot. You get these periods where the market gets so oversold that you just have relief rallies."

Relief rallies are not the same as recoveries. The distinction matters for anyone making capital allocation decisions right now.