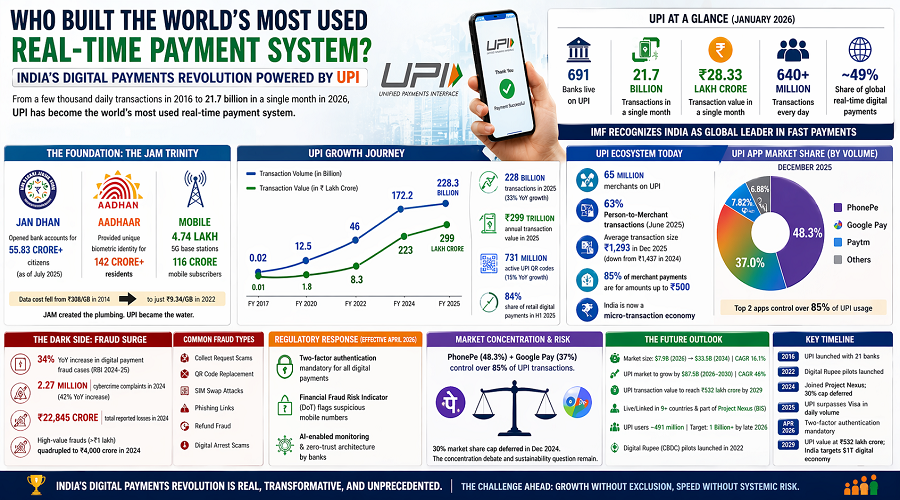

Who Built the World's Most Used Real-Time Payment System?

In 2016, the National Payments Corporation of India launched the Unified Payments Interface with 21 participating banks and a few thousand daily transactions. By January 2026, 691 banks were live on the network, processing 21.7 billion transactions in a single month, worth ₹28.33 lakh crore. No payment network in history has reached this scale this quickly.

The IMF formally recognized India as the global leader in fast payments. UPI now handles more than 640 million transactions every day, surpassing Visa's 639 million daily transactions. It accounts for approximately 49 percent of all real-time digital payment transactions globally.

This did not happen by accident. It was the product of a deliberate, decade-long infrastructure build. The Jan Dhan scheme opened bank accounts for over 55.83 crore citizens as of July 2025. Aadhaar provided a unique biometric identity for over 142 crore residents. India achieved one of the world's fastest 5G rollouts, with 4.74 lakh base stations active and a mobile subscriber base of 116 crore. The cost of mobile data fell from ₹308 per GB in 2014 to just ₹9.34 in 2022.

The Jan Dhan-Aadhaar-Mobile triad, the so-called JAM trinity, created the plumbing. UPI became the water that ran through it.

Key figures: UPI processed 228 billion transactions in 2025 (33% year-on-year growth), with an annual transaction value of ₹299 trillion. Active UPI QR codes reached 731 million. UPI's share of retail digital payments hit 84% in H1 2025. Market size in 2026 is projected at $7.9 billion, rising to $33.5 billion by 2034.

What Is Driving the Growth of Digital Payments in India?

India now has over 900 million internet users and over 500 million smartphone users. The convergence of mobile connectivity, financial inclusion, and a payment architecture that charges zero merchant fees for small transactions created the conditions for mass adoption.

The UPI ecosystem has reached 65 million merchants. The growth of QR code infrastructure solved the merchant-side problem that had stalled digital payments for years. Traditional point-of-sale terminals required hardware investment and maintenance. A QR code costs nothing to print. By 2025, UPI QR codes reached approximately 731.38 million active deployments, a 15 percent year-on-year increase. Neighbourhood shops, street vendors, and informal traders have embedded QR-based payments into daily commerce, which researchers at BCG call the Kirana effect.

The most telling data point in the 2025 numbers is the direction of ticket size. The average UPI transaction dropped to approximately ₹1,293 in December 2025, down from ₹1,437 in 2024. Within merchant payments, 85 percent of transactions were for amounts up to ₹500. India is evolving into a micro-transaction economy. When a roadside tea seller or vegetable vendor accepts UPI, cash is not being replaced at the top of the economy; it is being replaced at its base.

Person-to-merchant transactions captured 63 percent of all UPI transactions by June 2025, versus 37 percent person-to-person, a structural reversal from the platform's early years.

UPI transaction volume by year: FY 2017: 0.02 billion. FY 2020: 12.5 billion. FY 2022: 46 billion. FY 2024: 172.2 billion. FY 2025: 228.3 billion.

UPI app market share by volume (December 2025): PhonePe 48.3%, Google Pay 37.0%, Paytm 7.82%, all others 6.88%. The top two apps control over 85% of UPI usage.

Who Is Behind India's Digital Payment Fraud Surge?

The same speed and frictionlessness that made UPI extraordinary have become a structural liability. The RBI reported a 34 percent year-on-year increase in digital payment fraud cases in its 2024-25 Annual Report. Cybercrime complaints rose to 2.27 million in 2024, up 42 percent year-on-year, with total reported losses reaching approximately ₹22,845 crore. From 2.6 lakh reported incidents in 2021, the figure surged to nearly 28 lakh by 2025.

According to the Future Crime Research Foundation, most digital payment frauds today rely less on breaking systems and more on breaking human judgment. A hurried click on a malicious link or a casually shared OTP is often enough to drain an account within minutes.

Senior citizens lost more than ₹2,000 crore through impersonation and coercion-based scams. Younger users were targeted through fake job and income opportunities. Rural households suffered primarily from phishing-led UPI drains. High-value frauds above ₹1 lakh quadrupled to nearly ₹4,000 crore in 2024. The I4C reports that 80 percent of fraudulent activities originate from just 10 districts across India.

Common fraud types: Collect Request Scams, QR Code Replacement, SIM Swap Attacks, Phishing Links, Refund Fraud, and Digital Arrest Scams targeting senior citizens.

Regulatory response: From 1 April 2026, the RBI made two-factor authentication mandatory for all digital payments. The Department of Telecommunications launched a Financial Fraud Risk Indicator classifying suspicious mobile numbers as Medium, High, or Very High risk. Banks are now required to deploy AI-enabled monitoring and zero-trust architecture.

Who Controls the Infrastructure: Market Concentration and Regulatory Risk

PhonePe holds a 48.3 percent market share of UPI transactions by volume. Add Google Pay at 37 percent, and the top two apps control over 85 percent of a payment network that is now national infrastructure. The UPI market share cap for third-party apps, originally set at 30 percent, was deferred in December 2024 to avoid stalling innovation. That decision buys time but does not resolve the structural question: what happens if one dominant private player faces a regulatory or technical crisis?

The concentration debate plays into the monetization question. UPI's zero-fee model, subsidized by the government, has allowed rapid adoption but creates a sustainability problem. Banks process billions of transactions at significant infrastructure cost with limited revenue. The PwC Indian Payments Handbook 2025-2030 describes the next phase as one where "calibrated charges" become increasingly likely as banks' patience with zero-fee processing wears thin.

What Does the Future of India's Digital Payments Look Like?

The India digital payments market, valued at USD 6.83 billion in 2025, is projected to reach USD 33.5 billion by 2034, at a CAGR of 16.1 percent. The UPI market alone is expected to grow by USD 87.5 billion between 2026 and 2030, at a CAGR of 46 percent. By 2029, UPI transaction value is projected to reach ₹532 lakh crore.

UPI is already live or operationally linked in Singapore, UAE, Bhutan, Nepal, Sri Lanka, Qatar, France, and Mauritius. India joined Project Nexus in 2024, a Bank for International Settlements initiative expected to make UPI interoperable with real-time payment systems in Southeast Asia and beyond.

The RBI launched its wholesale Digital Rupee pilot on 1 November 2022 and retail pilot on 1 December 2022. The CBDC is designed not to compete with UPI but for quiet efficiency: addressing settlement risk, reducing leakages in welfare transfers, and facilitating offline payments in low-connectivity areas.

The current UPI user base of approximately 491 million is targeted to exceed one billion by late 2026. The path to that next 500 million runs through India's semi-urban and rural population first-time digital participants, feature phone users, and those for whom cyber literacy is still being built.

Key Timeline

2016 - UPI launches with 21 banks. Monthly volume: 17.86 million transactions.

2022 - RBI launches Digital Rupee pilot. Annual UPI transactions cross 46 billion.

2024 - India joins Project Nexus. 30% market share cap deferred. Annual volume: 172.2 billion. 2025 - UPI surpasses Visa in daily volume. Annual volume: 228.5 billion.

April 2026 - Mandatory two-factor authentication across all digital payment channels.

2029 - UPI transaction value projected at ₹532 lakh crore. India targets USD 1 trillion digital economy.

What the Numbers Really Mean

India's digital payments revolution is real, statistically verifiable, and changing everyday economic life for hundreds of millions of people. A street vendor in Kanpur who accepts QR payments now has a digital transaction record that can serve as a credit history. A migrant worker's family in a rural district can receive government benefits directly into a mobile-linked bank account. These are not marginal improvements. They are structural transformations.

But the same system that processes 698 million transactions every day also processes the fraudster's phishing link, the fake QR code, and the SIM-swap instruction. Cybercrime complaints grew 42 percent year-on-year in 2024. Whether the regulatory response is fast enough to match the velocity of an ecosystem processing nearly half of global real-time transactions is the open question that will define the decade ahead.

India's digital payments story is ultimately a story about what a country can build when policy, technology, and financial inclusion align. The infrastructure is world-class. The fraud challenge is real. The path to a billion users runs through some of the country's most digitally vulnerable citizens. Getting that combination right growth without exclusion, speed without systemic risk will determine whether India exports its payments model to the world or exports a cautionary tale alongside it.