The Bank of England has taken its most expansive financial stability action in years, extending its stress-testing framework beyond traditional banks into the fast-growing private credit and private equity sector. The move comes as global macroeconomic risks have increased, with the conflict in the Middle East triggering a substantial negative supply shock, large and volatile upward moves in global energy prices, and significant market reactions across the financial system.

What makes this round of testing different:

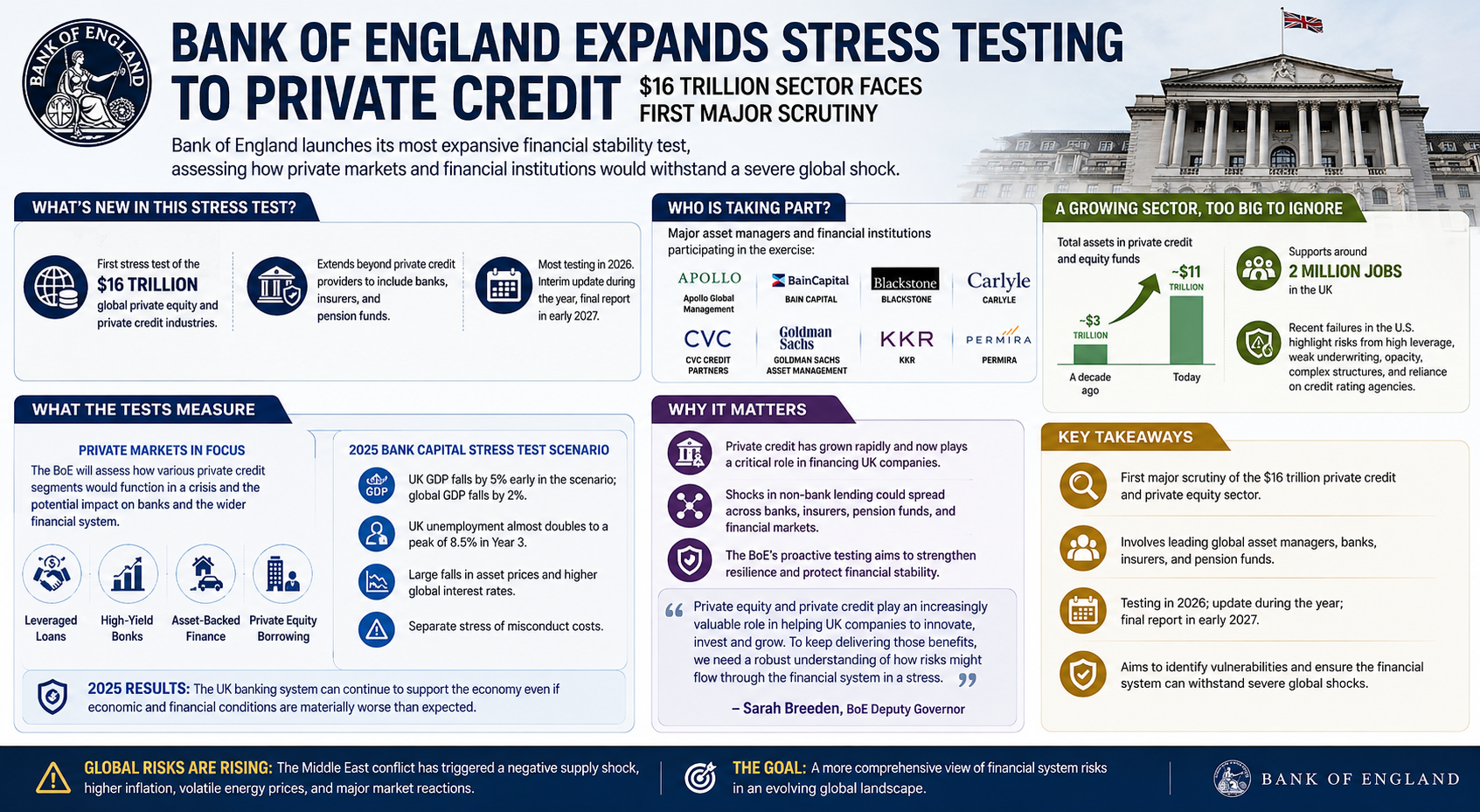

- The Bank launched a stress test of the $16 trillion global private equity and private credit industries to assess how they would deal with a major financial shock.

- The exercise, described as a system-wide exploratory scenario, extends beyond private credit providers to include banks, insurers, and pension funds.

- Most of the testing will happen in 2026, with the Bank expecting to give an update on its findings during the year before publishing a final report in early 2027.

Who Is Taking Part and What the Tests Actually Measure

Some of the alternative asset managers taking part include Apollo Global Management, Bain Capital, Blackstone, Carlyle, CVC Credit Partners, Goldman Sachs Asset Management, KKR, and Permira.

The Bank plans to assess various segments of private credit, including leveraged loans, high-yield bonds, asset-backed finance, and private equity borrowing, with the analysis focused on how these markets would function in a crisis and what effects this might have on banks and the broader financial sector.

On the traditional banking side, the 2025 Bank Capital Stress Test scenario tested:

- UK GDP falling by 5% in the early part of the scenario and world GDP falling by 2%.

- UK unemployment almost doubling to a peak rate of 8.5% in the third year.

- Large falls in asset prices, higher global interest rates, and a separate stress of misconduct costs.

The results of the 2025 Bank Capital Stress Test demonstrated that the UK banking system is able to continue to support the economy even if economic and financial conditions turn out to be materially worse than expected.

Why the Private Credit Sector Is Now Too Large for Regulators to Ignore

Total assets in private credit and equity funds have increased from around $3 trillion to $11 trillion over the past decade. They now play a major role in financing UK companies, with funding supporting around two million jobs.

BoE Governor Andrew Bailey said that the collapse of two large U.S. companies, car parts maker First Brands and auto dealership and lender Tricolor, showed how "high leverage, weak underwriting standards, opacity, complex structures, and the degree of reliance on credit rating agencies" could bite both banks and credit markets.

The FPC has maintained the UK countercyclical capital buffer rate at 2%, while noting that multiple vulnerabilities could be triggered at the same time, reinforcing the need for active risk management.

As BoE Deputy Governor Sarah Breeden put it: "Private equity and private credit play an increasingly valuable role in helping UK companies to innovate, invest and grow. To keep delivering those benefits, we need a robust understanding of how risks might flow through the financial system in a stress."